MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

Social inflation encapsulates how insurers' claims costs can rise above general economic inflation, and it also includes the shifts in societal preferences over who is best placed to absorb risk.

Unlike general economic inflation, which insurers can mitigate using pricing models and loss reserves, social inflation can arise from factors that are difficult to foresee, such as rising costs from:

The impact of these and other issues in the legal landscape can be intensified by third-party litigation funding.

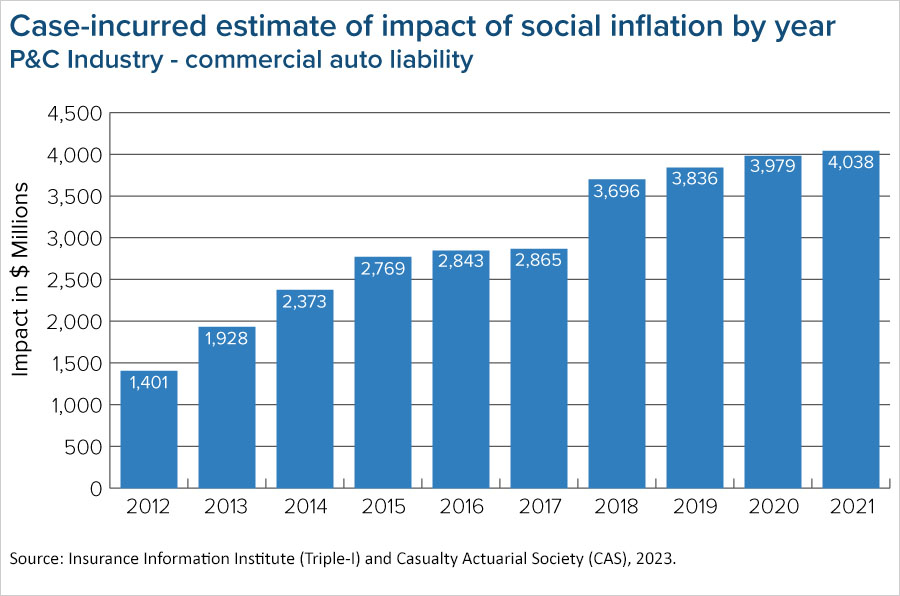

Social inflation drives higher insurer claim payouts and loss ratios. Ultimately, policyholders pay more for coverage. A simple way to think about social inflation and its components is to compare the impact of these factors on claims losses over time with growth in an inflation measure like the Consumer Price Index (CPI). The insurance lines that tend to bear the brunt are commercial auto, professional liability, product liability, and directors and officers liability. However, evidence indicates that pressure is mounting on private passenger automobile insurance, too.

Third-party litigation funding (TPLF) is a form of financing for legal expenses in which an investor provides money to attorneys or clients in exchange for a financial stake in the settlement or winnings of a lawsuit or arbitration. This money is often described as a non-recourse loan because it does not have to be repaid to the investor if the legal case is lost or never resolved. Also known as legal financing, legal funding, third-party litigation finance, or alternative litigation financing (ALF), this booming global industry is valued at $17 billion dollars and may expand to $30 billion by 2028, according to a Swiss RE report.

Research shows TPLF can contribute to social inflation by enabling more lengthy litigation, ultimately making insurance coverage more expensive. There are several other aspects of TLPF which can create concerns. We invite you to learn more in our white paper, “What is third-party litigation funding and how does it affect insurance pricing and affordability?

By increasing claims costs, social inflation threatens the affordability of insurance coverage. We are committed to advancing a solutions-oriented conversation involving insurers, policyholders, and policymakers (legislators, courts, regulators, etc.). Please join the discussion by reading more about our three-pillar mitigation strategy.

While social inflation remains hard to predict and mitigate, it is crucial to understand the factors at play and the risks to all stakeholders. We'll continue developing research and curating thought leadership resources to raise awareness. Follow our content here and our blog to stay abreast of this critical issue.